GitHub - Siam20Gangte/Auto-Regressive-models: Time Series Forecasting - ARIMA, SARIMA And Auto-ARIMA

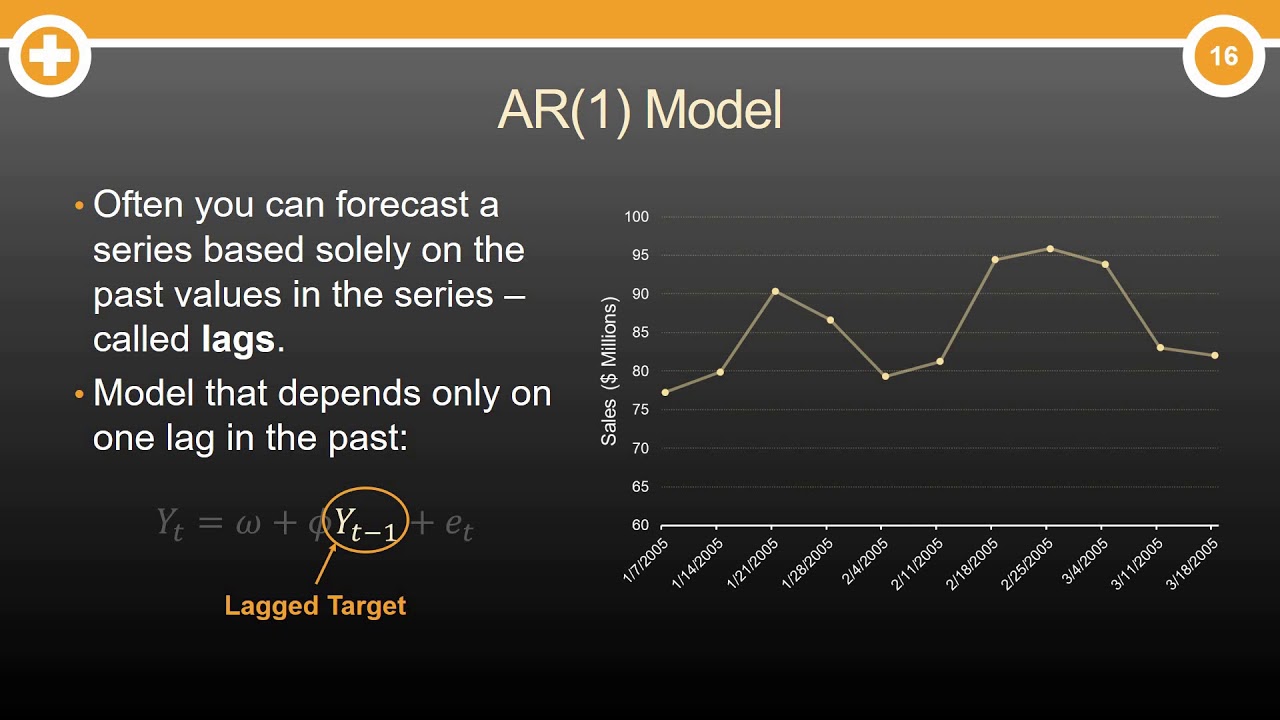

GitHub - Siam20Gangte/Auto-Regressive-models: Time Series Forecasting - ARIMA, SARIMA And Auto-ARIMA Autoregressive models vary based on the number of past values (lags) they use. the two most common types are: 1. ar (1) model: this is a autoregressive model of order 1 which is the simplest form of an autoregressive model. In statistics, econometrics, and signal processing, an autoregressive (ar) model is a representation of a type of random process; as such, it can be used to describe certain time varying processes in nature, economics, behavior, etc.

Simple Auto-Regressive Models Shown To Be Powerful Universal Learners

Simple Auto-Regressive Models Shown To Be Powerful Universal Learners What is an autoregressive model? an autoregressive (ar) model predicts future behavior based on past behavior. it’s used for forecasting when there is some correlation between values in a time series and the values that precede and succeed them. Auto regressive models aim to predict a time series by relying exclusively on its previous values, also known as lags. they are based on the assumption that the current value of a time series variable depends linearly on its past values. Auto regressive models | ar1 ar2 ar (p) models watch the full class time series cfa l2: • cfa level 2 | time series analysis pa for more videos please subscribe to the channel: /. Autoregressive models are expressed as dependence on lagged values. these types of models are generally good are modeling stationary processes that move forward in time. first order ar models ar (1) and second order ar models ar (2) are discussed first.

PPT - Auto-regressive Dynamical Models PowerPoint Presentation, Free Download - ID:281126

PPT - Auto-regressive Dynamical Models PowerPoint Presentation, Free Download - ID:281126 Auto regressive models | ar1 ar2 ar (p) models watch the full class time series cfa l2: • cfa level 2 | time series analysis pa for more videos please subscribe to the channel: /. Autoregressive models are expressed as dependence on lagged values. these types of models are generally good are modeling stationary processes that move forward in time. first order ar models ar (1) and second order ar models ar (2) are discussed first. We use the term autoregression since (1) is actually a linear. regression model for xt in terms of the explanatory variable xt 1 . that is, xt is being modeled as a. regression on its own past. we will see that x . ε t is uncorrelated with past values of the ar series t. or innovations . Auto regressive (ar) model in microsoft excel.ar (1), ar (2) and ar (3) models.interpretation and finding the best fit model.time series analysis.time series re. Hello fellow modelers, and welcome to my current list! on this list, call or write with a want list. want lists are always accepted and kept on file for kits you particularly need. i will contact you if the kit becomes available. In general, given a set of conditionals p(yijyj; j 6= i), there does not necessarily exist a joint distribution p(y1; :::; yn) with those conditionals. what to do about non gaussian data?.

PPT - Auto-regressive Dynamical Models PowerPoint Presentation, Free Download - ID:281126

PPT - Auto-regressive Dynamical Models PowerPoint Presentation, Free Download - ID:281126 We use the term autoregression since (1) is actually a linear. regression model for xt in terms of the explanatory variable xt 1 . that is, xt is being modeled as a. regression on its own past. we will see that x . ε t is uncorrelated with past values of the ar series t. or innovations . Auto regressive (ar) model in microsoft excel.ar (1), ar (2) and ar (3) models.interpretation and finding the best fit model.time series analysis.time series re. Hello fellow modelers, and welcome to my current list! on this list, call or write with a want list. want lists are always accepted and kept on file for kits you particularly need. i will contact you if the kit becomes available. In general, given a set of conditionals p(yijyj; j 6= i), there does not necessarily exist a joint distribution p(y1; :::; yn) with those conditionals. what to do about non gaussian data?.

What are Autoregressive (AR) Models

What are Autoregressive (AR) Models

Related image with auto regressive models ar1 ar2 arp models

: Autoregressive Models")

Models With Regular And | Chegg.com")

To (f) Corresponding To The Labeled AR(p) Models, Compare The... | Download Scientific Diagram")

Related image with auto regressive models ar1 ar2 arp models

Models")

Models")

Models: Mean reversion, Covariance Stationarity")

About "Auto Regressive Models Ar1 Ar2 Arp Models"

Comments are closed.